India's Semiconductor Manufacturing in 2026–2030: PLI Impact, Global Standing, and AI-Era Policy Needs

How India's PLI scheme is building semiconductor capacity, what it means for global supply chains, and what government must do next as AI demand reshapes the industry.

14 min read

Semiconductors-Policy in India

India's PLI scheme commits $10 billion to build semiconductor manufacturing capacity over 5 years, with TATA and Micron fab projects expected to deliver 1–2 million wafers monthly by 2027. By 2030, India could claim 2–3% of global semiconductor production - a major jump from today's <1%, though still far behind Taiwan and South Korea.

Geopolitically, this matters: as supply chains de-risk away from Taiwan and China, India becomes a critical third hub for mature-node and memory-chip manufacturing. However, success hinges on three critical gaps the government must address.

First: Execute land acquisition and power supply for fabs without further delays. Second: Ramp AI-specific semiconductor manufacturing, not just mature logic and memory - India's AI startups need domestic chip design capacity. Third: Fund advanced-node R&D now to avoid a 5-year technology gap by 2030.

Alone, PLI is a solid foundation. With aligned AI policy and proactive R&D investment, India becomes a genuine semiconductor power by 2035.

Understanding PLI: India's $10B Semiconductor Bet

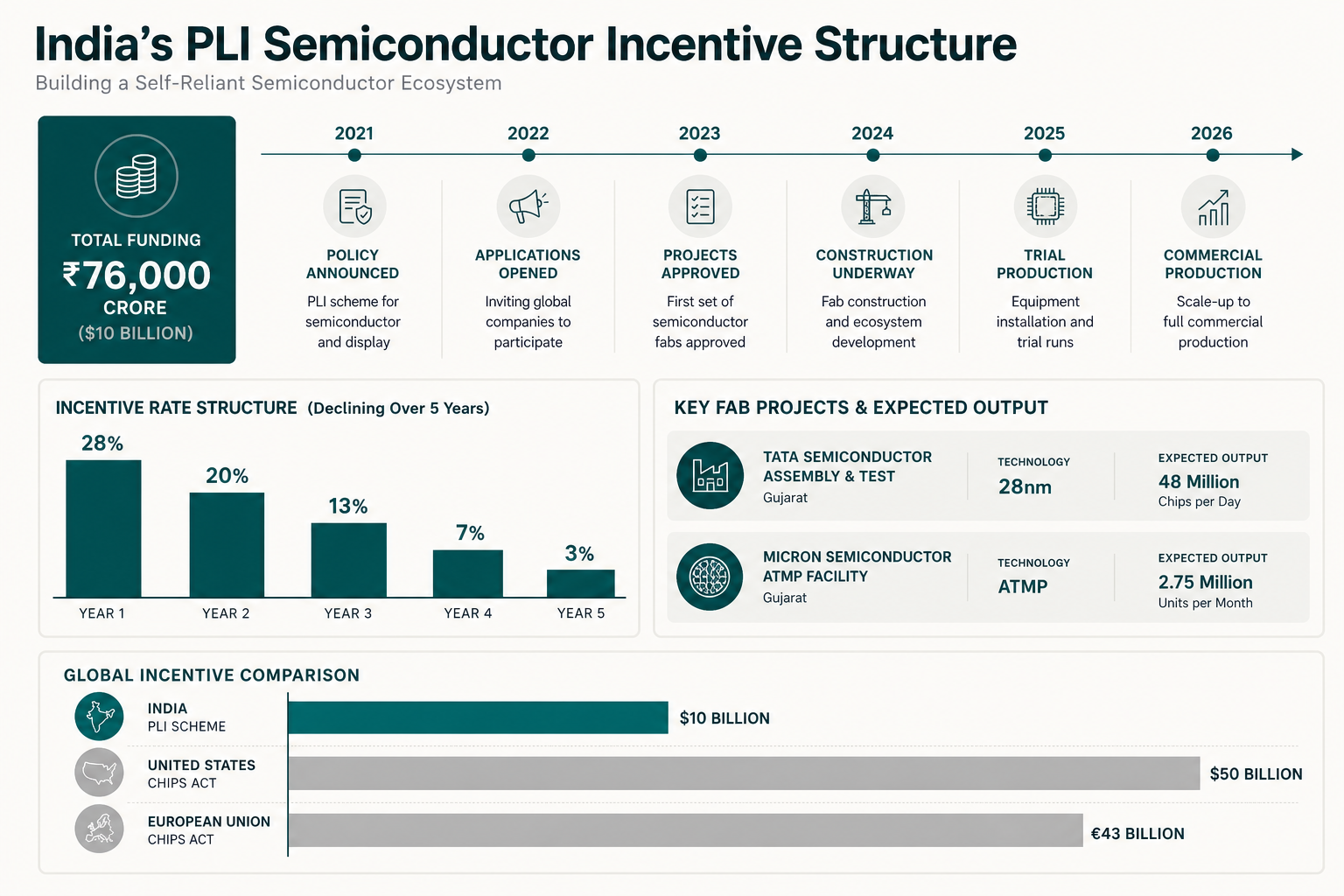

The Production-Linked Incentive (PLI) scheme launched in 2021 with an audacious goal: turn India into a semiconductor manufacturer at scale. The government put ₹76,000 crore ($10 billion USD) on the table, betting that cash incentives could attract multinational players to build fabs on Indian soil.

Here's how it works: companies that invest at least ₹1,000 crore (~$120M) in a semiconductor fab and hit annual sales milestones receive up to 28% of incremental sales as a direct payment from the government. A company selling $100 million in semiconductors annually would get $28 million back from the scheme. For a capital-intensive business with thin margins, this is meaningful.

The incentives are structured to decline over time - higher in years 1–3, stepping down in years 4–5 - pushing companies to become profitable on their own merits eventually.

TATA Semiconductor (backed by Singapore's Foxconn partnership) is building a ₹18,000 crore (~$2.2 billion) fab in Dholera, Gujarat, targeting 28nm and mature nodes. Micron Technology committed to a DRAM and NAND memory fab in Sanand, Gujarat, with ₹3,700+ crore capex. Smaller players - IIT-Delhi backed semiconductor labs, compound semiconductor startups - are also ramping up under PLI.

The timeline matters: both major projects faced delays (land acquisition, environmental approvals), but are now in active construction. By 2026, India expects at least 2–3 semiconductor fabs in early production.

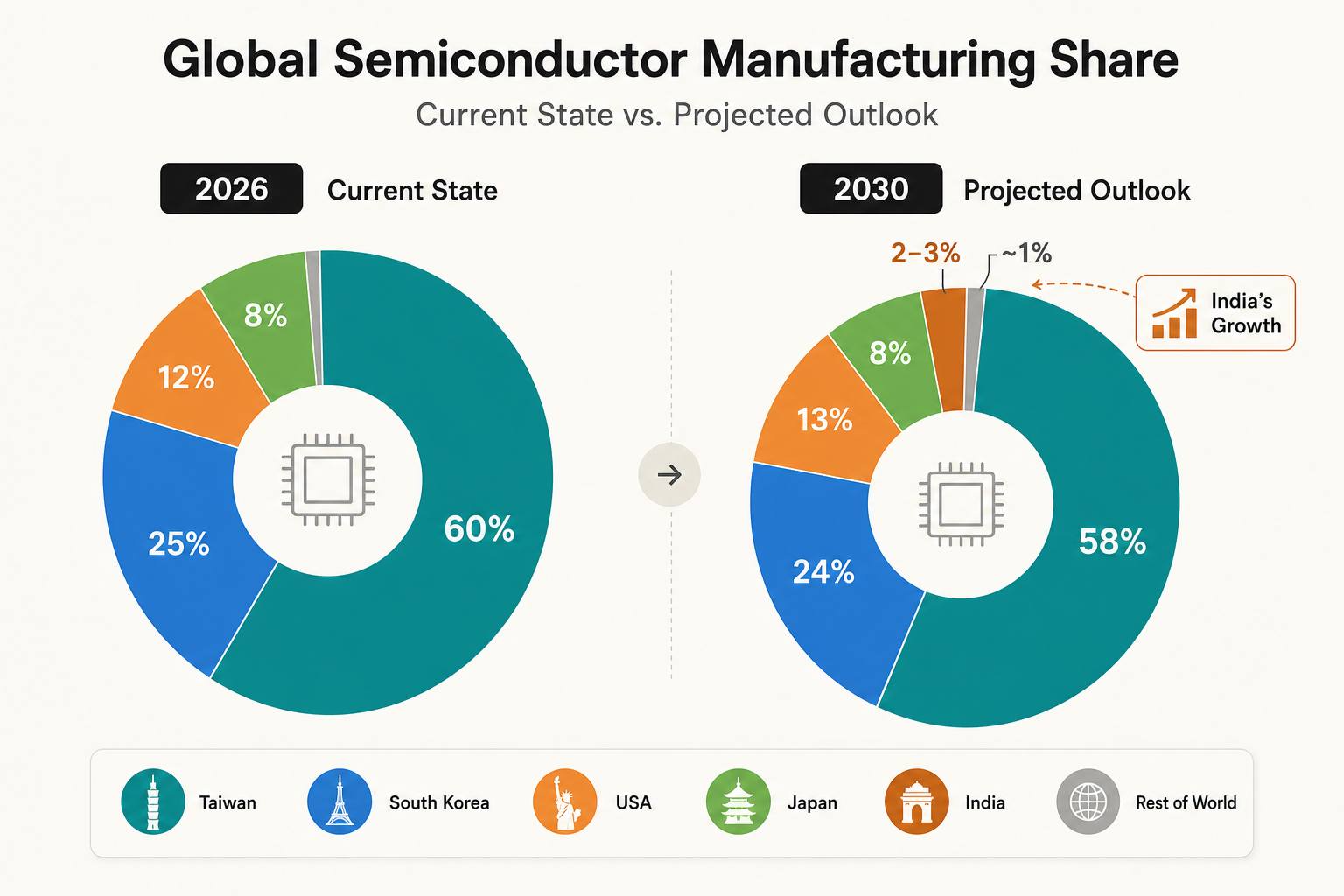

India's Global Standing in 2028–2030: The 2–3% Scenario

Today, India manufactures less than 1% of the world's semiconductors. By 2030, if PLI executes as planned, this could be 2–3%.

| Region/Country | 2026 Share | 2030 Projection |

|---|---|---|

| Taiwan | ~60% (advanced logic) | ~58% |

| South Korea | ~25% | ~24% |

| United States | ~12% | ~13% |

| Japan | ~8% | ~8% |

| India | <1% | 2–3% |

| Rest of world | ~3% | ~2% |

India's growth is real but proportional: it's not replacing Taiwan or South Korea. Instead, India is capturing the lucrative middle: mature nodes (28nm and above) and memory chips - the least expensive fabs to build, but still highly profitable.

Why does this matter globally?

1. Supply-chain de-risking after Taiwan concentration

TSMC dominates advanced chip production with 54% market share. If Taiwan faces conflict or supply disruption, the entire world's advanced-chip supply breaks. Companies and governments are now actively building alternatives.

India becomes a second source for mature nodes. Samsung, Micron, and TATA producing in India means Nvidia, Apple, and Microsoft can source certain chips (memory, analog, RF, older-generation logic) from non-Taiwan fabs. It's insurance.

2. Geopolitical hedging by US allies

The US views India as a critical partner - strategically aligned, willing to reduce China dependence, and less risky than Taiwan. Under the CHIPS and Science Act, the US is willing to fund semiconductor capacity in allied nations. India qualifies, and access to US capital and IP becomes more fluid.

Japan and South Korea also see India as a hedge against relying solely on each other or the US.

3. AI demand is reshaping the entire supply chain

AI model training and inference require enormous amounts of memory and specialized accelerators. Nvidia GPUs, TPUs, and inference processors are in extreme shortage. Memory chip demand (HBM, GDDR6X) is spiking.

Micron's India facility comes online right as memory demand explodes. Similarly, demand for mature-node analog and RF chips (used in power management, signal processing) is surging due to AI infrastructure build-out.

India isn't just capturing market share - it's arriving at the exact moment the market desperately needs capacity.

2026–2030: The PLI Execution Timeline

Now to end-2026: FAB construction and ramp

- TATA Gujarat fab: Now in active construction; first chip expected late 2025 to early 2026. Ramp-up to 50,000 wafers per month by end-2026.

- Micron Sanand: Similarly in ramp phase; targeting 100,000+ wafer starts monthly by end-2026.

- Specialty semiconductor makers: Compound semiconductor (GaN, SiC) initiatives ramping at smaller scale.

Risks: Land acquisition delays (ongoing in Gujarat), power supply negotiations, water availability. All solvable, but execution has been messier than planned.

2027–2028: Production at scale

- Combined capacity: TATA + Micron + others = 1.5–2 million wafers per month (mature nodes)

- Incremental production: ~2–3 billion chips annually (mature nodes, memory)

- PLI payout: Government disbursing ₹2,000–5,000 crore annually to incentivize further capex

2029–2030: India becomes a top-5 semiconductor producer

- Production share: 2–3% globally

- Export value: ~$1–2 billion annually in mature nodes, memory, specialty chips

- Employment: 20,000–30,000 direct jobs in fabs; 50,000–100,000 indirect jobs across supply chain

- Geopolitical status: India recognized as critical semiconductor hub alongside Taiwan, South Korea, US

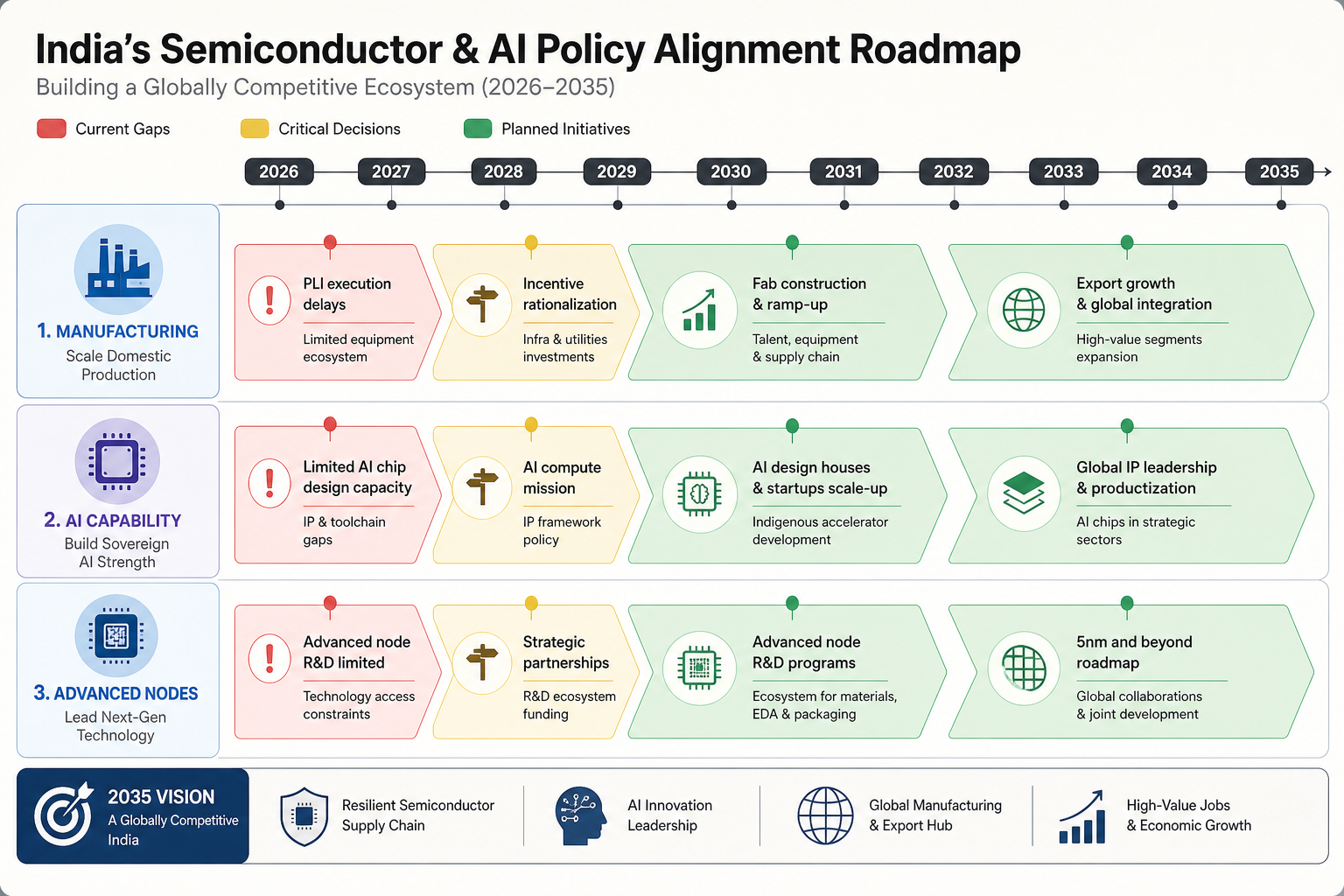

The Gaps: What India's PLI Doesn't Cover

PLI is working, but it has three blind spots.

Gap 1: AI and semiconductor misalignment

India is investing heavily in AI - funding startups, building IIT research, training engineers. Simultaneously, it's building semiconductor capacity via PLI. But the two aren't connected.

India's AI strategy is software-focused: models, datasets, talent. The semiconductor piece? It assumes imports. Indian AI startups will still buy GPUs from Nvidia (US company, TSMC-made). Indian cloud providers will source memory and accelerators globally.

The problem: If the US restricts chip exports to India, India's AI independence evaporates instantly - despite billions invested in software.

What's missing:

- Domestic GPU and AI accelerator design capability (India has none)

- PLI extension to include AI-specific chips (tensor processors, inference accelerators)

- Government-backed R&D for Indian semiconductor design houses

- Partnerships with Nvidia, Qualcomm to establish design centers in India

Gap 2: No advanced-node roadmap

PLI targets mature nodes (28nm and above). That's profitable and sensible for now. But by 2030, the global semicon market will be increasingly AI-driven, and AI increasingly uses advanced nodes (5nm, 7nm) for efficiency.

TSMC's cutting-edge fabs are booked years out. Samsung is expanding. Intel is recovering via the US CHIPS Act. India has no public roadmap for 5nm manufacturing.

The US CHIPS Act is funding 5nm+ fabs in Arizona and Ohio. The EU is backing TSMC and Intel in Europe. China is racing to close the gap. India is silent on advanced nodes.

What's missing:

- Government commitment to 5nm/7nm production target (2032–2035)

- Tech-transfer partnerships with TSMC or Samsung (needs negotiation)

- Additional R&D funding beyond PLI incentives

- IP frameworks that allow partnerships without surrendering sovereignty

Gap 3: Skill pipeline bottleneck

A modern fab requires thousands of engineers and technicians - fab operators, process engineers, quality technicians, maintenance specialists. These roles require 4–6 years of specialized training.

India doesn't have enough. Training programs exist (NASSCOM, ITIs), but they're overwhelmed. TATA and Micron are recruiting globally, offering premium salaries to lure talent from Taiwan, South Korea, and the US.

What's missing:

- Fast-track apprenticeships and bootcamps (5,000+ trained annually by 2028)

- University curriculum changes in IITs and NITs to emphasize fab operations

- Tax incentives for experienced fab engineers to relocate to India

- Government-backed partnerships with TSMC and Samsung training academies

Policy Moves: What Government Must Do Next

The PLI foundation is solid. To capitalize on 2026–2030 momentum, India needs three more policy pushes.

Action: Launch a ₹5,000 crore (~$600 million) "India Semiconductor Design Institute" (ISDI), modeled on Belgium's IMEC or France's CEA-LETI.

Focus:

- Indigenous AI chip design (GPUs, TPUs, inference accelerators)

- Advanced packaging and heat management for dense chips

- R&D partnerships with Nvidia, Qualcomm, AMD for design know-how

Outcome by 2030: 5–10 Indian semiconductor design startups shipping custom AI chips; India's role shifts from pure manufacturing to design + manufacturing.

Move 2: Fast-track 5nm roadmap

Action: Announce a public commitment to 5nm production by 2034 (with execution metrics). Negotiate with TSMC or Samsung for joint-venture fab in India.

Rationale:

- US CHIPS Act is creating 5nm capacity in Arizona by 2026. EU is backing similar moves. China is racing. India cannot afford to be absent.

- 2034 is realistic (4–5 years of construction + ramp); earlier creates execution risk.

Funding: Additional ₹10,000–15,000 crore beyond PLI (new budget line).

Outcome by 2035: India has 5nm production capacity; not world-leading, but not lagging.

Move 3: Aggressive talent pipeline

Action: Fund 5,000 fab technician and engineer slots annually in government-backed boot camps (partnership with existing training providers).

Details:

- 6–12 month intensive programs

- Apprenticeships with TATA and Micron (paid)

- Post-training job placement guarantees

- Tax breaks for experienced engineers relocating to India

Outcome by 2028: India has 30,000+ trained fab technicians; dependency on foreign recruitment drops.

Competitive Reality: Where India Stands vs. US, China, EU

India is moving faster than any country in building new capacity. PLI is effective. Execution so far is... mixed but improving.

However:

- The US CHIPS Act ($50B) is larger and more generous

- China is subsidizing heavily and has existing advanced-node know-how

- The EU's €43B Chips Act is better-funded and includes advanced nodes

- Taiwan still dominates (TSMC's competitive advantage is nearly impossible to replicate)

India's advantage is cost and geopolitical positioning, not technology leadership. A fab in India will always be cheaper to operate than one in Arizona or Germany. And India's alignment with the US makes it preferred for sensitive supply chains.

By 2030, India's role is clear: Critical secondary hub for mature nodes and memory, helping diversify away from Taiwan and China. Not a leader in advanced nodes, but essential for resilience.

The Opportunity: AI Accelerates India's Timeline

Here's where India got lucky: AI demand is reshaping which chips matter most, and India is positioned to benefit.

Advanced training requires massive memory (HBM - expensive, advanced-node dependent). But inference - running existing models - uses mature nodes, memory, and accelerators. As AI pushes inference to the edge (phones, IoT, data centers worldwide), demand for mature-node and memory manufacturing explodes.

Micron's India facility targets exactly this - high-volume memory production. TATA targets mature nodes and specialty chips. Both directly benefit from the AI wave.

If the government aligns AI policy with semiconductor manufacturing - funding design houses, extending PLI to AI accelerators, partnering with Nvidia on India-based design and production - India could become the global hub for AI inference chips by 2035.

That's a $50+ billion opportunity, and it's reachable.

The Next 3–5 Years: What Success Looks Like

By 2027

- TATA fab producing 50,000+ wafers/month

- Micron ramping memory production

- 15,000–20,000 fab jobs created

- Export revenue: $200–500 million

By 2028

- Combined India capacity: 1–1.5 million wafers/month

- India recognized as top-5 semiconductor producer globally

- PLI disbursements: ₹3,000–5,000 crore annually

- Skill training: 10,000+ technicians trained annually

By 2030

- India at 2–3% global semiconductor share

- Second major fab (advanced node or specialty) operational

- AI accelerator design capability emerging (startups shipping products)

- Export revenue: $1–2 billion annually

- India as critical supply-chain hedge for US, Japan, South Korea

By 2035 (if advanced-node roadmap executes)

- India at 3–5% global share

- 5nm fab operational

- Indigenous GPU/AI accelerator design competitive globally

- Semiconductor exports: $5–10 billion annually

The Bottom Line

PLI is India's smartest economic bet in decades. It's building real capacity, at the exact moment the world needs semiconductor resilience.

The execution risk is real - fab construction is hard, skills are scarce, timelines slip. But the geopolitical wind is at India's back: the US, Japan, and allies are actively wanting India to succeed as a non-China, non-Taiwan source.

For India to truly capitalize, three things must happen: Execute the fabs without further delays. Align AI policy with semiconductor manufacturing. Fund advanced-node R&D now.

Do those three, and India transitions from a semiconductor afterthought to a genuine strategic player by 2035. Fail on any one, and the moment passes - China and the US will dominate, and India returns to importing.

The choice is India's to make. The market is waiting.

Comments

Post a Comment