Why crowds are almost always wrong: the data behind herd mentality and market cycles

The crowd is a terrible investor. DALBAR data, SEBI studies, and a century of market cycles show why - and what it means for how we think.

July 11, 2026 · 12 min read

TL;DR

The crowd is a poor investor - and we have 30 years of data to prove it. DALBAR's 2024 study shows the average equity investor trailed the S&P 500 by 848 basis points last year. SEBI's 2024 study shows 93% of Indian F&O traders lost money between FY22 and FY24. This isn't incompetence - it's the predictable result of how human psychology functions under social pressure. Understanding why crowds are systematically wrong is more useful than any specific investment thesis.

The most dangerous consensus in a room is the one nobody questions

There is a moment, in every market bubble, that looks identical in retrospect but feels completely different in the moment. It is the moment when the crowd stops asking "is this worth buying?" and starts asking "why hasn't everyone bought this yet?"

The question sounds like due diligence. It is actually its opposite. The moment collective validation replaces individual analysis, you are no longer in an information market - you are in a social one. And social markets have their own logic, which has very little to do with underlying value.

This shift is not rare or exotic. It happens in every market cycle, at every scale, across centuries and continents. Tulip bulbs in 17th century Amsterdam. Railroad shares in 1840s Britain. Technology stocks in 1999. Real estate in 2006. Crypto in 2021. F&O contracts in present-day India. The specific asset changes. The human mechanism underneath does not.

What herd behaviour actually is - and why it's individually rational

The standard framing is that herd behaviour is irrational. This is wrong, and the error matters.

John Maynard Keynes diagnosed the core problem in 1936 with his famous beauty contest analogy. In a newspaper contest where readers guess which photograph other readers will find most beautiful, the winning strategy is not to pick the most beautiful face - it is to pick the face you think others will think is most beautiful. Layered social inference, not fundamental judgment, is the optimal play.

The same logic governs stock markets. Investors who buy when others are buying are not simply being foolish. They are, in many cases, making a rational decision given the information available to them: other people are buying this, which is itself a signal that someone with better information has made a positive judgment. The error is in how far they carry this inference - and how many cascades of inference stack on top of each other before prices detach entirely from fundamentals.

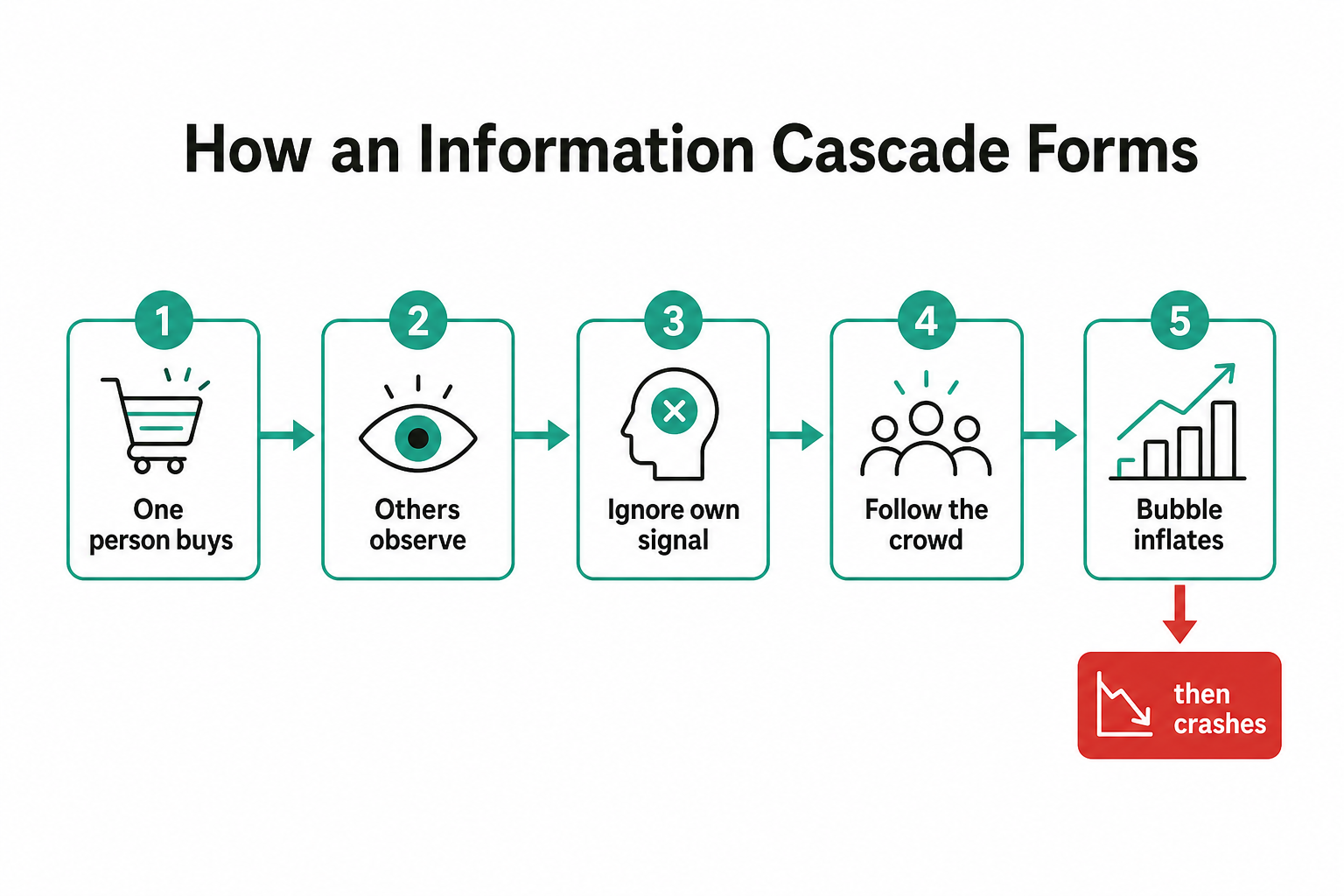

Bikhchandani, Hirshleifer, and Welch formalised this in 1992 in their landmark paper on information cascades. Their core finding: when enough people before you have made the same decision, it is mathematically rational to ignore your own private information and follow them - even when the cascade is based on a mistake made early in the chain. The cascade is self-reinforcing until it breaks. And when it breaks, it breaks fast.

The paradox Bikhchandani identified is that herding can be individually rational and collectively catastrophic at the same time. Each actor may be behaving sensibly given what they observe. The aggregate behaviour, built from those individually sensible decisions, creates a price that is completely divorced from value.

The behavioural architecture underneath the herd

Understanding why the cascade forms requires going one level deeper into the psychological machinery that runs beneath conscious analysis.

Daniel Kahneman's research separates human cognition into two systems. System 1 is fast, automatic, and heavily social - it reads the room, calibrates to what others are doing, and generates instant intuitive responses. System 2 is slow, deliberate, and analytical - it's where independent judgment lives. The problem: System 2 requires cognitive effort. Under conditions of uncertainty, time pressure, or social conformity, System 1 takes over. And System 1, in ambiguous situations, defaults to what the group is doing.

Robert Shiller's narrative economics adds another layer. Shiller's central argument is that economic decisions are not primarily driven by data or analysis - they are driven by stories that spread virally through populations. "Tech companies will transform everything" in 1999. "House prices only go up" in 2005. "DeFi will replace banks" in 2021. These are not conclusions drawn from evidence. They are socially contagious narratives that rational people adopt because everyone around them has adopted them.

Richard Thaler's work on nudges shows how social defaults encode group behaviour into individual choices without anyone noticing. When "investing in X" becomes the default action of your peer group, opting out requires active resistance - and most people, under normal social pressure, do not resist defaults.

Three additional mechanisms accelerate the cascade once it begins:

Loss aversion. Kahneman and Tversky's foundational research established that the psychological pain of a loss is approximately twice the pleasure of an equivalent gain. FOMO - the fear of missing out on gains others are making - triggers loss aversion even before any actual loss has occurred. The crowd's success is itself experienced as a form of loss by those outside it.

Social proof. The crowd's behaviour functions as information. When thousands of people are buying an asset, the observer's implicit inference is "they must know something." This is often false - but it is a reasonable prior in the absence of independent information.

Availability bias. Recent, vivid stories about gains - the neighbour who made 5x on GameStop, the colleague who doubled their money in F&O - are cognitively over-weighted relative to the more accurate base rates. The stories that circulate are the success stories. The 93% who lost money are quieter.

The data: what happens to the crowd

The theoretical argument for why crowds are wrong is compelling. The empirical data is damning.

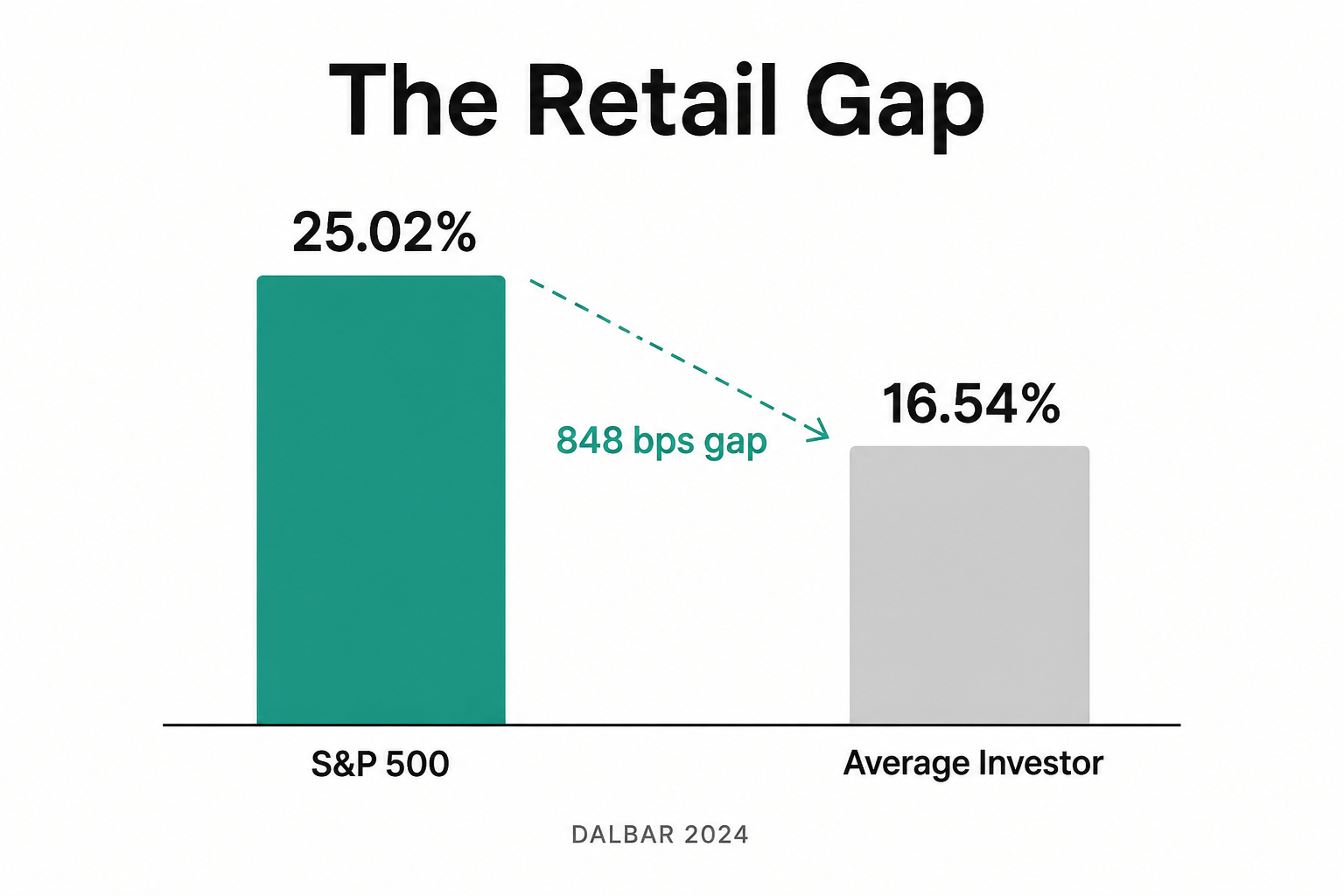

The DALBAR gap

DALBAR's Quantitative Analysis of Investor Behavior, running for over 30 years, compares what markets return with what the average retail investor actually receives. The gap exists entirely because of behavioural errors: buying after rallies, selling during crashes, chasing recent performance.

In 2024, the average equity investor earned 16.54% while the S&P 500 returned 25.02% - an 848 basis point gap, the second-largest ever recorded. In 2023, the gap was 5.5%. Over a 20-year horizon, DALBAR estimates the average retail investor has underperformed the S&P 500 by approximately 6% annually. Compounded over two decades, that gap is not a rounding error - it is the difference between financial security and regret.

The mechanism is consistent: retail investors, as a group, systematically buy high (when the crowd is euphoric) and sell low (when the crowd is panicking). The crowd's collective action defeats its collective interest.

The dot-com destruction

The Nasdaq rose 86% in 1999 alone. The crowd's thesis was simple: anything with a ".com" suffix was valuable because the internet was going to transform everything. This was not entirely wrong - the internet did transform everything. The crowd's error was in paying any price, for any company, regardless of revenue, profitability, or coherent business model.

When the tide turned in 2000, the Nasdaq fell 78% from peak to trough by October 2002, erasing $4.4 trillion in market value. It took 15 years for the Nasdaq to recover its previous high. The crowd that piled in during 1999 and 2000 - the people for whom the narrative was most compelling - absorbed the worst of those losses.

The GameStop inversion

January 2021 offered a novel variant: a crowd that assembled intentionally, on Reddit's r/wallstreetbets, to collectively target a heavily-shorted stock and engineer a short squeeze. The strategy was explicit, coordinated, and self-aware. GameStop moved from roughly $20 to $483 in weeks.

A study published in Nature found that Reddit activity had statistically significant predictive power over GameStop's intraday price movements - the crowd was, briefly, the market. Melvin Capital, a hedge fund that had heavily shorted GME, lost 53% of its investments by the end of January 2021.

What happened to the retail crowd? Most who bought above $100 lost heavily when the squeeze reversed. The crowd beat a specific set of institutional investors in a specific window. Then the crowd lost to itself - later entrants, who joined after the price had already risen dramatically, absorbed losses as the original momentum faded. The herd ate its own tail.

"In the herd, investors often lose their individual investing decision-making, dropping their accessibility and analysis of information in favour of following the crowd."

The Indian case study: F&O and the democratisation of self-destruction

No contemporary data set illustrates the herd dynamic more starkly than India's F&O market.

India's Demat account count surged from approximately 40 million in 2020 to over 170 million by 2025. COVID-era retail participation, combined with zero-commission brokers, social media communities, and YouTube traders showing highlight-reel returns, created an enormous wave of new market participants. A large portion migrated to Futures & Options - leveraged derivatives that amplify both gains and losses.

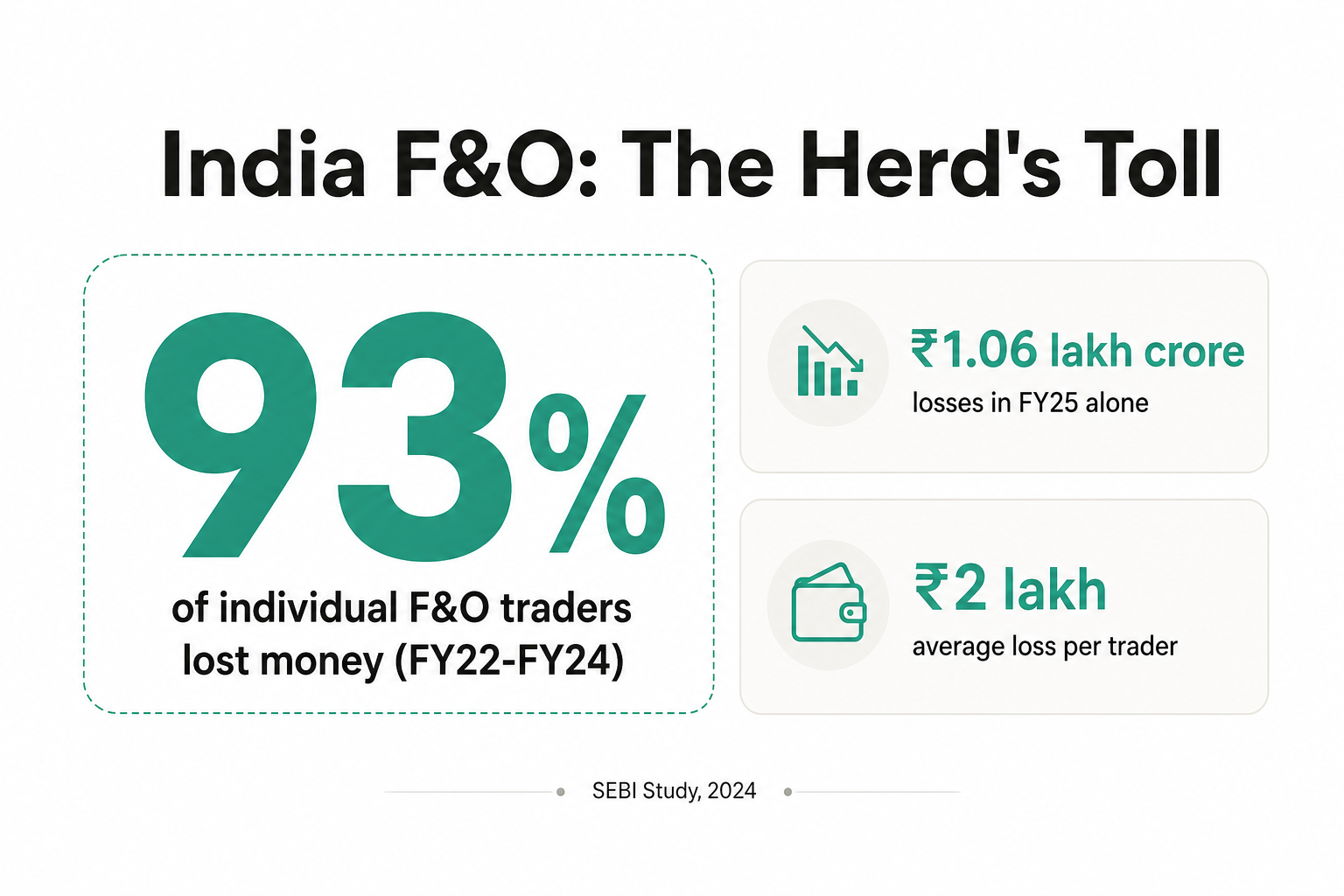

The outcome is documented in precise detail. SEBI's September 2024 study found:

- 93% of over 1 crore individual F&O traders incurred losses between FY22 and FY24

- Average loss per trader: approximately ₹2 lakh

- In FY25 alone: net individual losses of ₹1,05,603 crore - up 41% from ₹74,812 crore in FY24

The mechanism is textbook herd behaviour. New retail participants entered F&O because others appeared to be making money. Social media amplified the success stories and muted the failures. The availability bias ran at full strength - the visible winners felt more representative than the invisible majority losing ₹2 lakh a year.

The crowd grew larger. The losses grew proportionally. This is not a story about financial illiteracy - the SEBI data includes traders who continued actively for multiple years. It is a story about the structural disadvantage of entering a zero-sum leveraged market driven by social momentum rather than informational edge.

Why the crowd's timing is always wrong

There is a structural reason the crowd tends to enter at the wrong moment, not just a psychological one.

Price movements attract attention. Attention attracts coverage. Coverage attracts new participants. New participants push prices higher. Higher prices attract more attention. The feedback loop is self-sustaining - right up until it isn't.

By the time a market move is large enough and sustained enough to generate broad social awareness and emotional resonance, the majority of the move has already happened. The late-entering crowd is paying elevated prices for an asset whose momentum is already attracting the attention of people looking to take profits. The crowd's arrival is often closer to the top than to the bottom.

Investopedia's summary captures the mechanism: herd instinct "has a history of starting large, unfounded market rallies and sell-offs that are often based on a lack of fundamental support to justify either." The unfunded rally is the crowd buying what has already risen. The unfunded sell-off is the crowd selling what has already fallen.

Keynes identified the solution - and why it is so psychologically uncomfortable to execute. In his beauty contest framing, the sophisticated investor is not the one who best predicts what the group will do, but the one who identifies, early enough, what the group has not yet realised. Acting on that judgment requires being visibly wrong for a period, which activates the exact social and psychological pressures that push most investors toward the crowd in the first place.

The contrarian is not romantic - they are just early

The correct response to this data is not nihilism about markets, or a romantic attachment to contrarianism for its own sake. Contrarians are wrong too - often, and for extended periods.

What the data supports is a more precise claim: the crowd is a reliable late-cycle indicator. Not a contrary signal in real time, but a clear marker that a thesis has become mainstream and therefore priced. When a narrative has spread broadly enough that a DALBAR-style retail investor has acted on it, the information content of that narrative has largely been captured by the market. The remaining price upside, if any, is smaller. The downside, amplified by the number of investors now holding the same position, is larger.

This is, for what it is worth, exactly what Warren Buffett's famous maxim encodes: be fearful when others are greedy, be greedy when others are fearful. The maxim sounds simple. The psychological difficulty of executing it is the reason it describes the exception rather than the rule.

We are social animals. Social conformity is not a bug in our cognition - it was adaptive for most of human history. The problem is that markets are one of the few environments where our social instincts reliably produce worse outcomes than solitary, uncomfortable, independent analysis.

The data on this is not ambiguous. Across 30 years of DALBAR research, across the arc of every major bubble and crash, across SEBI's documentation of India's F&O reality - the crowd's collective financial wisdom consistently falls short of what a passive, unemotional index would have returned to them without any effort at all.

The crowd is, almost always, wrong. Not because the individuals in it are foolish, but because the dynamics of crowd formation guarantee that the information they are acting on is, by the time they act on it, already old news.

Understanding that - really internalising it, not just knowing it - is the beginning of thinking independently about anything: markets, politics, trends, or the narratives that spread through social systems and pass for common sense. We are what we are. But we can at least know what we are doing.

Sources

- DALBAR - Investors Missed the Best of 2024's Market Gains

- Investopedia - Herd Instinct

- Investopedia - Dotcom Bubble

- SEBI Study - 93% of Individual Traders Incurred Losses in Equity F&O FY22–FY24

- Moneycontrol - SEBI study: Individual investors down 20% in F&O trading

- Wikipedia - GameStop Short Squeeze

- Nature - The dynamics of the Reddit collective action leading to the GameStop short squeeze

- Goldman Sachs - The Late 1990s Dot-Com Bubble

- Nobel Prize - Daniel Kahneman

- Nobel Prize - Robert Shiller

- Nobel Prize - Richard Thaler

- io-fund - Retail Investors Take the Brunt of Market Losses

- JSTOR - Information Cascades (Bikhchandani, Hirshleifer, Welch)

- ResearchGate - Herding Mentality in the GameStop Short Squeeze

Frequently Asked Questions

What is herd mentality in investing?

Herd mentality in investing refers to the tendency of individuals to follow the crowd - buying when others are buying and selling when others are selling - rather than relying on independent analysis. It is driven by psychological forces including FOMO, social proof, and loss aversion. At scale, it creates asset bubbles and market crashes.

Does the average investor actually underperform the market?

Yes, consistently. DALBAR's 2024 QAIB study found the average equity investor earned 16.54% vs the S&P 500's 25.02% - an 848 basis point gap. Over 20 years, DALBAR estimates retail investors have underperformed the market by roughly 6% annually. The gap is almost entirely explained by behavioural errors: buying high, selling low, and chasing momentum.

What percentage of F&O traders in India lose money?

SEBI's September 2024 study found that 93% of over 1 crore individual F&O traders incurred losses between FY22 and FY24, with an average loss of approximately ₹2 lakh per trader. In FY25 alone, individual traders lost ₹1,05,603 crore in the F&O segment - a 41% increase over the prior year.

What are the biggest historical examples of herd behaviour in markets?

The most studied cases are: Tulip Mania (1634-37), where a single tulip bulb sold for the price of a craftsman's annual wage; the Dot-com bubble (1995-2002), where the Nasdaq rose 86% in 1999 alone before falling 78%; the 2008 Global Financial Crisis, driven by collective assumptions about housing prices; and the GameStop short squeeze (2021), where Reddit-coordinated retail buying pushed a stock from $20 to $483 before the reversal. Each demonstrates the same pattern: crowd momentum divorced from underlying value.

How can someone avoid herd behaviour in investing?

The practical moves: (1) do your own analysis before acting on market noise; (2) impose a waiting period before reacting to crowd-driven price moves; (3) separate your investment thesis from price action - if the company's fundamentals haven't changed, neither should your position; (4) take note of when everyone around you agrees that something is obviously true - that consensus is often when contrarian returns are highest. Behavioural economists recommend pre-committing to rules that override in-the-moment social pressure.

Comments

Post a Comment